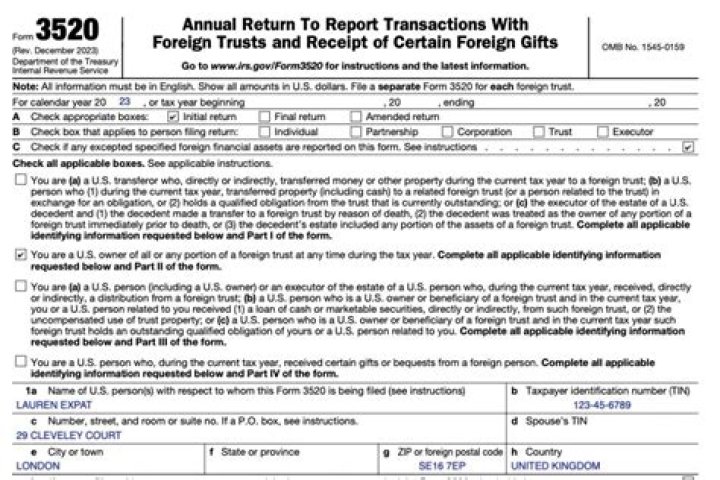

Who needs to file Form 3520 A?

Form 3520-A is needed if a foreign trust exists with a US owner, and a US beneficiary receives a distribution from a foreign trust. The foreign trust must furnish the required annual statements; otherwise, the US owner or beneficiary must complete and attach Form 3520-A to its Form 3520.

Do I need to file a 3520?

Form 3520 for U.S. recipients of foreign gifts You’re only required to file this form if you received: A gift of more than $100,000 from a foreign person or estate. A gift of more than $15,601 from a foreign partnership or corporation.

What do you need to know about Form 3520?

U.S. persons (and executors of estates of U.S. decedents) file Form 3520 to report: Certain transactions with foreign trusts, Ownership of foreign trusts under the rules of sections 671 through 679, and Receipt of certain large gifts or bequests from certain foreign persons.

Do you have to file a Form 3520 for a foreign gift?

The Form 3520 is technically referred to as the Annual Return To Report Transactions With Foreign Trusts and Receipt of Certain Foreign Gifts. Not everyone who is a US person and receives a gift from a foreign person will have to file the Form 3520.

When to file Form 3520 for foreign trusts?

U.S. persons (and executors of estates of U.S. decedents) file Form 3520 to report: Certain transactions with foreign trusts. Ownership of foreign trusts under the rules of sections Internal Revenue Code 671 through 679. Receipt of certain large gifts or bequests from certain foreign persons.

How to file Form 3520 for an executor?

However, if you are an executor filing a Form 3520 with respect to a U.S. decedent, provide both the name of the Service Center where the decedent’s final income tax return will be filed, and the name of the Service Center where Form 706 will be filed, if applicable. Please enter the information as follows.