Why allowance method is preferred?

The allowance method is preferred over the direct write-off method because: The income statement will report the bad debts expense closer to the time of the sale or service, and. The balance sheet will report a more realistic net amount of accounts receivable that will actually be turning to cash.

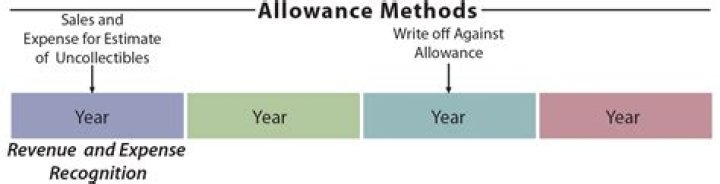

What is the direct write-off method and the allowance method?

The direct write-off method recognizes bad accounts as an expense at the point when judged to be uncollectible and is the required method for federal income tax purposes. The allowance method provides in advance for uncollectible accounts think of as setting aside money in a reserve account.

Which is better the direct write-off method or the allowance method?

The direct write-off method is an easier way of treating the bad debt expense since it only involves a single entry where bad debt expense is debited and accounts receivable is credited. The allowance method is more complicated since it requires you to create a provision account which is a contra-asset account.

Why isn’t the direct write off method accepted under GAAP?

The GAAP prohibits direct write-off because it doesn’t conform to the matching principle, which requires that every transaction affecting one account, such as inventory, be matched with another account, such as cash.

Why is the direct write off method not acceptable to GAAP?

The Direct Write off Method and GAAP GAAP mandates that expenses be matched with revenue during the same accounting period. This distortion goes against GAAP principles as the balance sheet will report more revenue than was generated. This is why GAAP doesn’t allow the direct write off method for financial reporting.

Is the direct write off method allowed under GAAP?

The direct write off method doesn’t comply with the GAAP, or generally accepted accounting principles. GAAP states that expenses and revenue must be matched within the same accounting period.