Why am I taxed twice on Social Security?

It’s a “contribution,” not a tax. This allows the IRS to tax you on the money you put into Social Security and the money you receive out as a benefit — because on the way out, it’s technically not a tax.

Can Sallie Mae garnish Social Security?

Yes — and the government may not wait until you’re nearing retirement age to recoup the debt. If you default on federal student loans, the government can take extreme measures to get your money. For example: The government can tell your employer to withhold your pay.

Is your Social Security tax free?

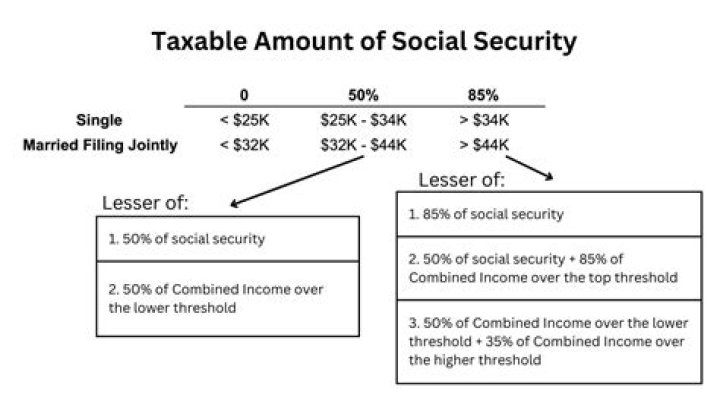

Nobody pays taxes on more than 85 percent of their Social Security benefits, no matter their income. For purposes of determining how the Internal Revenue Service treats your Social Security payments, “income” means your adjusted gross income plus nontaxable interest income plus half of your Social Security benefits.

What is the income limit for Social Security deductions?

For 2021 that limit is $18,960. In the year you reach full retirement age, we deduct $1 in benefits for every $3 you earn above a different limit, but we only count earnings before the month you reach your full retirement age.

When do you get paid for Supplemental Security income?

Supplemental Security Income (SSI) follows a different payment schedule — it’s paid on the 1st of each month. We’ll take a detailed look at the different Social Security payment schedules, including the exact payment dates for 2021.

What’s the maximum amount you can make on social security before Fra?

In the calendar year you reach FRA, which you can check out on our website, you have a higher earnings limit. Additionally, we will only count earnings for the months prior to FRA. In 2017, the limit was $44,880. In 2018, it is $45,360. In the year of FRA attainment, Social Security deducts $1 in benefits…

When do you get deducted from your Social Security benefits?

In the year of FRA attainment, Social Security deducts $1 in benefits for every $3 you earn above the limit. There is a special rule that usually only applies in your first year of receiving retirement benefits.