How do you explain standard deduction?

The standard deduction is the portion of income not subject to tax that can be used to reduce your tax bill. You can choose between a standard deduction and itemized deductions. The amount of your standard deduction is based on your filing status, age, and other criteria.

What are valid tax deductions?

You subtract deductions from your gross income and sometimes, you’ll end up in a lower tax bracket as a result. Popular tax deductions include the student loan interest deduction, the medical expenses deduction, the IRA contributions deduction and the self-employment expenses deduction.

Do I need receipts for all tax deductions?

The Internal Revenue Service allows you to deduct expenses that are ordinary and necessary for the operation of your business. However, if you are audited, you need to show receipts for these deductions. So, you should keep receipts for everything you plan to write off when you file taxes for your business.

Can you deduct 300 in charitable contributions without itemizing?

Following special tax law changes made earlier this year, cash donations of up to $300 made before December 31, 2020, are now deductible when people file their taxes in 2021. Under this new change, individual taxpayers can claim an “above-the-line” deduction of up to $300 for cash donations made to charity during 2020.

What is a good standard deduction?

All tax filers can claim this deduction unless they choose to itemize their deductions. For the 2020 tax year, the standard deduction is $12,400 for single filers and $24,800 for joint filers. Filers who have a head of household status get a deduction of $18,650.

What is the limit for standard deduction for salaried employees?

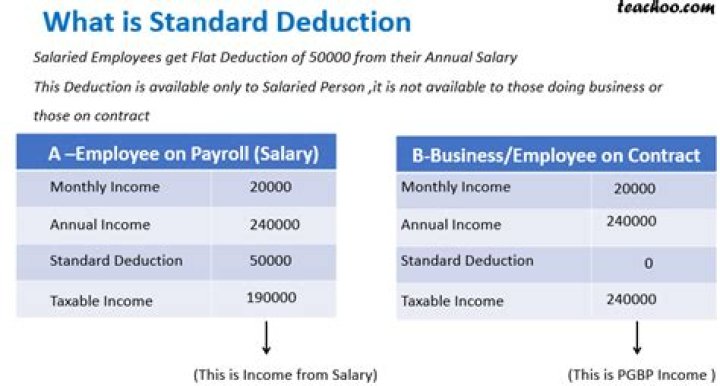

Maximum Limit for Standard Deduction. 1 Salaried individuals can claim standard deduction up to Rs 50,000 on their income. 2 Pensioners can claim Rs. 50,000 or their total annual pension as standard deduction, whichever is lower.

How is the amount of the standard deduction determined?

The amount of your standard deduction is based on your filing status, age, and other criteria. Income tax is the amount of money that the federal or state government takes from your taxable income. It is important to note that taxable income and total income earned for the year are not the same.

What is the limit of standard deduction in India?

Standard deduction means a flat deduction to individuals earning salary or pension income. It was introduced back in Budget 2018 in lieu of exemption of transport allowance and reimbursement of miscellaneous medical expenses. For the FY 2019-20 & FY 2020-21 the limit of the standard deduction is Rs 50,000. Latest News

What is the standard deduction for income for 2018?

If you are a single tax filer with gross income of $80,000 for 2018, you can reduce your income by $12,000 to taxable income of $68,000. Your tax bill for income of $68,000 would be $10,905 or an effective tax rate (ETR) of 16.03%. If you paid taxes on the entire $80,000, your bill would be $15,535, or an ETR of 19.42%.