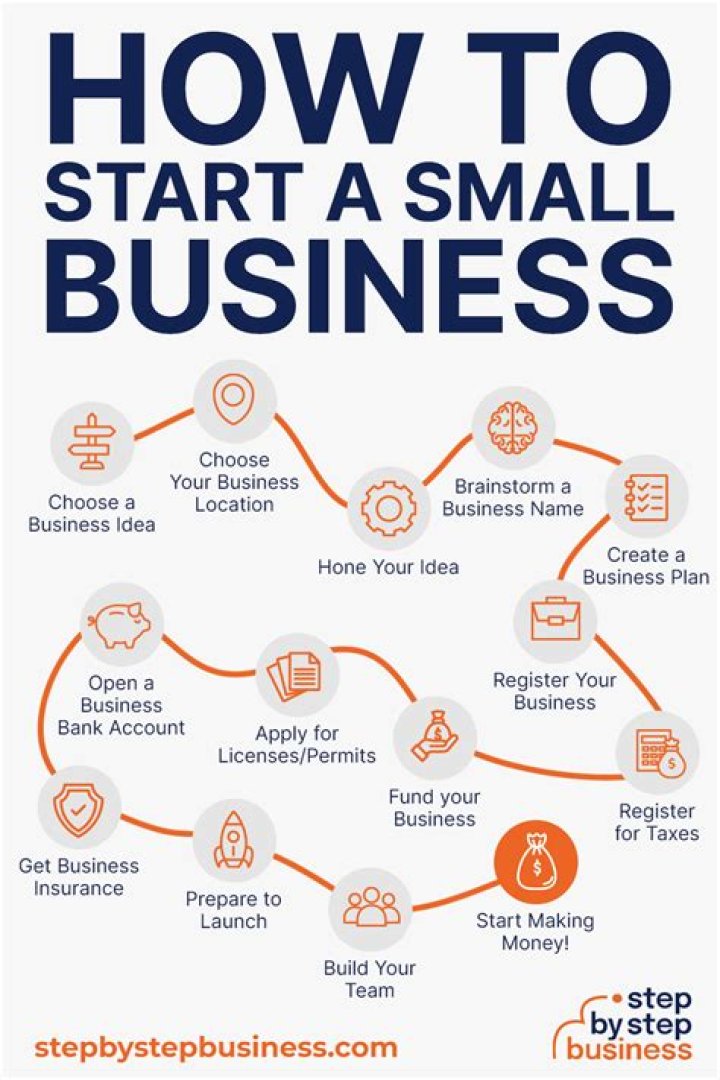

What costs do you incur when starting a business?

Startup costs are the expenses incurred during the process of creating a new business. Pre-opening startup costs include a business plan, research expenses, borrowing costs, and expenses for technology. Post-opening startup costs include advertising, promotion, and employee expenses.

What is an example of that one time start-up cost?

One-time expenses are the initial costs needed to start the business. Buying major equipment, hiring a logo designer, and paying for permits, licenses, and fees are generally considered to be one-time expenses.

Do more new businesses succeed or fail after 5 years?

It’s often said that more than half of new businesses fail during the first year. Data from the BLS shows that approximately 20% of new businesses fail during the first two years of being open, 45% during the first five years, and 65% during the first 10 years. Only 25% of new businesses make it to 15 years or more.

What are examples of running cost?

The running costs of a business are the amount of money that is regularly spent on things such as salaries, heating, lighting, and rent.

Can you claim company setup costs?

Under normal circumstances startup costs are regarded as a capital cost of a business and not tax-deductible. Because you are conducting your business from home, unless you can find a way that substantiates your claim for electricity and gas related to running the business, you cannot claim these costs.

Is running a charge?

Charges that are directly related to the cost of production, generally figured on per M basis. It can include materials, press time, other machine operations and miscellaneous labor.

What are start-up costs?

Start-up costs can be defined fairly simply as the expenses that are incurred during the process of setting up a company. Generally, things like advertising, office furnishings, damage deposits, and so on are all considered to be pre-launch costs.

What do you need to know about startup costs?

To qualify as startup costs, the costs must be ones that could be deducted as business expenses if incurred by an existing active business and must be incurred before the active business begins (Sec. 195 (c) (1)).

When do startup costs not include interest and taxes?

Startup costs do not include costs for interest, taxes, and research and experimentation (Sec. 195 (c) (1)). Once a taxpayer decides to acquire a particular business, the costs to acquire it are not startup costs (Rev. Rul. 99 – 23 ), and the taxpayer must capitalize the acquisition costs (Sec. 263 (a) and INDOPCO, Inc., 503 U.S. 79 (1992)).

When to deduct start-up costs and organizational expenses?

Start-up Costs and Organizational Expenses Are Deducted over 180 Months Investigating the potential for a new business and getting it started can be an expensive proposition. However, you can’t deduct these expenses under the general rules for business deductions because only expenses for an existing trade or business can be deducted.

Do you underestimate the cost of starting a business?

Underestimating expenses falsely increases expected net profit, a situation that does not bode well for any small business owner. Careful research of the industry and consumer makeup must be conducted before starting a business. Some business owners choose to hire market research firms to aid them in the assessment process.