What is the built-in gains holding period?

The holding period for short-term capital gains and losses is generally 1 year or less. The holding period for long-term capital gains and losses is generally more than 1 year. However, an exception applies for certain sales of applicable partnership interests.

How are built-in gains calculated?

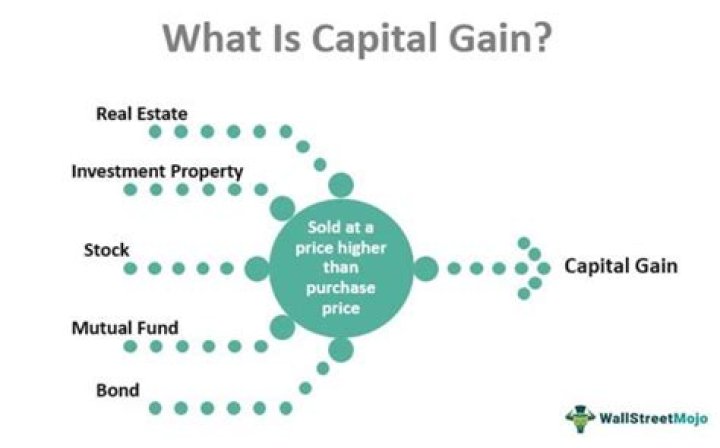

To calculate the built-in gains tax, you will need to determine both short-and-long-term C corporation assets. Subtract the adjusted basis of the assets from their fair market value. Only if the adjusted basis number is higher than the fair market value will you have to pay the built-in gains tax.

How long is the recognition period?

The “permanent” recognition period is the 10-year period beginning with the first day of the first tax year for which the corporation was an S corporation. 16 Under the regulations, a “10-year period” is 120 months; 17 short tax years do not reduce the 10-year recognition period.

Overview of built-in gains tax The built-in gains (BIG) tax generally applies to C corporations that make an S corporation election, and it can be assessed during the five-year period beginning with the first day of the first tax year for which the S election is effective.

How do you calculate built-in gains?

Calculating the Built-in Gains Tax Subtract the adjusted basis of the assets from their fair market value. Only if the adjusted basis number is higher than the fair market value will you have to pay the built-in gains tax.

How is built-in gain taxed?

The corporation must determine whether it has a net unrealized built-in gain in its assets on the effective date of the relevant transaction. Built-in gains recognized during this period are taxed at the highest rate of tax applicable to corporations (currently 35%).

What is built-in gain property?

Summary. The built-in gains tax is a corporate-level tax on gain from certain property sales made in the recognition period following an S election by a C corporation. This gain is generally referred to as net recognized built-in gain.

When is a holding period considered a long-term gain?

The holding period after which the IRS considers an investment a long-term gain (or loss) for tax purposes. Long-term capital gains are taxed at a more favorable rate than short-term gains. When an investor receives a stock dividend, the holding period for the new shares, or portions of a new share, is the same as for the old shares.

How to calculate holding period for an under construction property?

You will have to make many calculations and will be liable to pay tax, especially during transactions. So when selling such property, holding period becomes critical in deciding the taxation benefit on the long-term capital gain. Here is what you all need to know about the term: What is holding period?

When does the holding period start and end?

Starting on the day after the security’s acquisition and continuing until the day of its disposal or sale, the holding period determines tax implications. For example, Sarah bought 100 shares of stock on Jan. 2, 2016.

When does the built in gain carry forward?

However, any built – in gain not recognized because of the taxable income limitation carries forward during the remainder of the recognition period and is recognized in a later year to the extent there is taxable income (Sec. 1374 (d) (2); Regs. Sec. 1. 1374 – 2 (c)).