What is the purpose of an unearned revenue account?

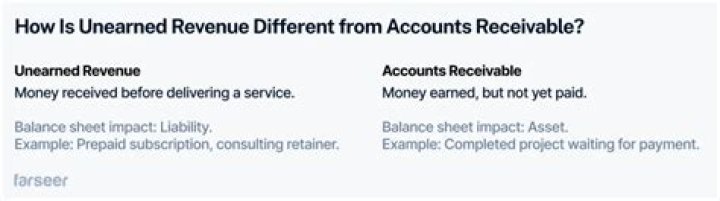

unearned revenue(s) definition. A liability account that reports amounts received in advance of providing goods or services. When the goods or services are provided, this account balance is decreased and a revenue account is increased. To learn more, see Explanation of Adjusting Entries.

How do you explain unearned income?

Unearned revenue is money received by an individual or company for a service or product that has yet to be provided or delivered. It can be thought of as a “prepayment” for goods or services that a person or company is expected to supply to the purchaser at a later date.

What is unearned service income?

Unearned Service Revenue is a liability account that is used to record advanced collections from clients of a service type business. In other words, it pertains to revenue already collected but the service has not yet been rendered. Also known as: Advances from Customers or Customer’s Advances.

Unearned revenue is money received by an individual or company for a service or product that has yet to be provided or delivered. It is recorded on a company’s balance sheet as a liability because it represents a debt owed to the customer.

When to use unearned revenue and deferred income?

Under the liability method, a liability account is recorded when the amount is collected. The common accounts used are: Unearned Revenue, Deferred Income, Advances from Customers, etc. For this illustration, let us use Unearned Revenue. Suppose on January 10, 2020, ABC Company made $30,000 advanced collections from its customers.

What does it mean to adjust entry for unearned revenue?

Adjusting Entry for Unearned Revenue. Unearned revenue (also known as deferred revenue or deferred income) represents revenue already collected but not yet earned. Hence, they are also called “advances from customers”.

How are earned income and unearned income determined?

The IRS determines your responsibility to file based on your gross income, which consists of both earned and unearned income. This is especially important if you can be claimed as a dependent on someone else’s tax return. Your eligibility for certain tax credits and IRA contributions also depends on how much earned income you have.

When to use unearned income as a retirement supplement?

Unearned income can serve as a supplement to earned income before retirement and, often, is the only source of income in post-retirement years. During the accumulation phase, taxes are deferred for many sources of unearned income.